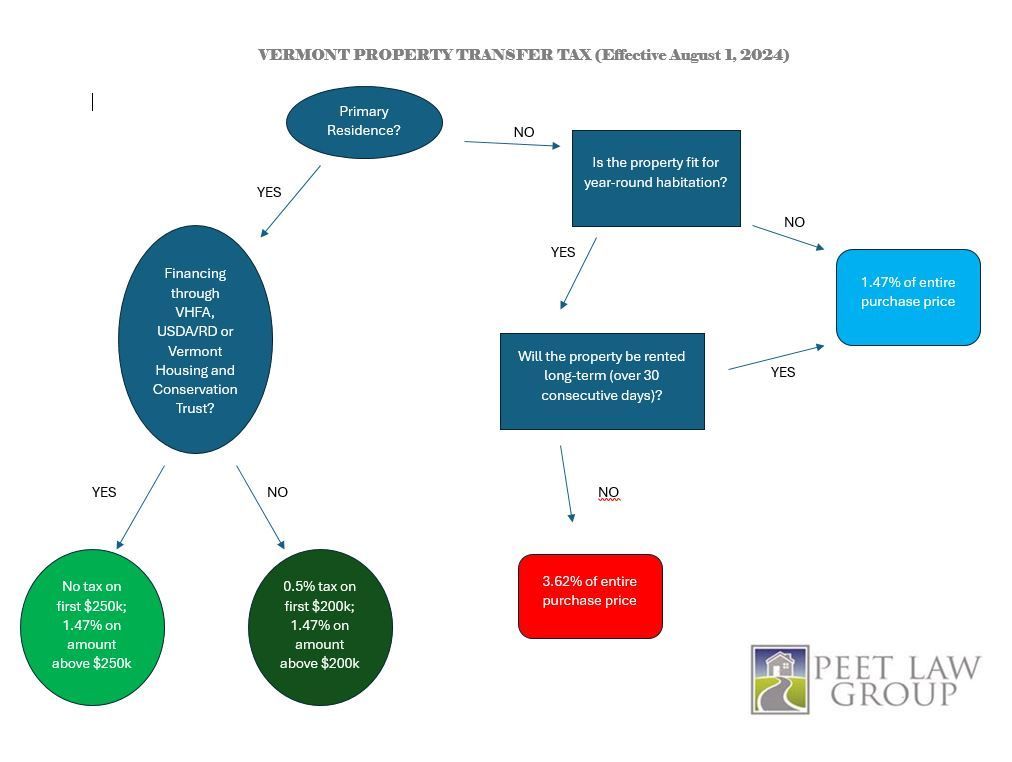

How Much is the Vermont Property Transfer Tax?

A Step-by-Step Flow Chart to Calculate Transfer Tax

Our team at the Peet Law Group is ready to assist you with any questions about transfer taxes. Feel free to call or email us at 802-860-4767 or office@peetlaw.com.

Learn what to review before closing on a Vermont condo purchase, including resale certificates, special assessments, association finances, insurance, rules, and more.

Learn what closing costs Vermont home buyers pay, including transfer tax, title insurance, attorney fees, lender costs, escrow deposits, and more.

Why Every Married Vermont Homeowner Should Understand Tenancy by the Entirety

Buying or Selling a Home in Vermont? Here's What Happens After the Contract Is Signed

A Delaware Statutory Trust Can Help You Defer Capital Gains Taxes While Transitioning From Active Property Management to Passive Real Estate Ownership

Buying vacant land in Vermont? Learn about zoning, septic permits, Current Use, Act 250, wetlands, flood zones, financing, and other essential due diligence tips before you buy.

Learn how Vermont attorneys resolve title defects, clear liens, address deed issues, and help buyers and sellers reach a successful closing.

Making a Home Purchase Offer in Vermont: Key Terms, Contingencies, and Legal Considerations

Common Title Search Surprises We Have Found After Thousands of Vermont Title Searches

Essential Legal Services Every First-Time Home Buyer in Vermont Should Understand